基于逻辑回归的银行贷款全流程实战

基于逻辑回归的银行贷款全流程实战

前言

在数字金融高速发展的今天,信用卡欺诈已成为全球银行与支付机构面临的核心风险之一。据相关行业统计,每年因信用卡欺诈造成的经济损失高达数百亿美元,且欺诈手段日趋智能化、隐蔽化,传统基于规则引擎的风控系统已难以应对复杂多变的欺诈模式。

信用卡欺诈检测本质上是一个二分类任务,但它具备两个极具挑战性的特点:

- 样本极度不平衡:正常交易占比超过99.7%,欺诈交易不足0.3%;

- 误判代价极不对称:漏判欺诈(FN)会直接造成资金损失,误判正常交易(FP)会影响用户体验。

因此,在欺诈检测场景中,准确率毫无意义,我们更关注少数类(欺诈)的召回率、精确率与F1值。

本文以经典Kaggle信用卡交易数据集为基础,从零开始实现一套完整的逻辑回归欺诈检测流程,内容涵盖:

- 逻辑回归数学原理与公式推导

- Sklearn逻辑回归参数深度解析

- 数据预处理、标准化、EDA可视化

- 样本不平衡问题分析与处理思路

- 模型训练、交叉验证、超参数搜索

- 混淆矩阵、分类报告、阈值优化

- 完整可运行代码+详细注释

一、逻辑回归核心原理精讲

1.1 什么是逻辑回归

逻辑回归(Logistic Regression)名为回归,实为分类,是统计学与机器学习中最经典、最常用的线性二分类模型,广泛应用于金融风控、疾病预测、广告点击率预估等场景。

它的核心思想非常简洁:

在线性回归的输出基础上,套一层Sigmoid函数,将任意实数映射到(0,1)区间,从而将输出解释为样本属于正类的概率。

1.2 从线性回归到逻辑回归

线性回归模型:

z=θ0+θ1x1+θ2x2+⋯+θnxn=θTx z = \theta_0 + \theta_1 x_1 + \theta_2 x_2 + \dots + \theta_n x_n = \boldsymbol{\theta}^T \boldsymbol{x} z=θ0+θ1x1+θ2x2+⋯+θnxn=θTx

线性回归的问题:

- 输出范围为(-∞,+∞),无法表示概率;

- 无法直接用于分类任务。

为了解决这个问题,逻辑回归引入Sigmoid函数。

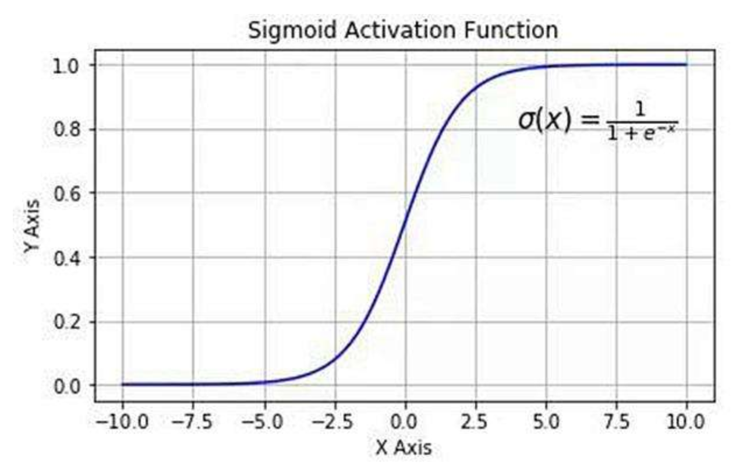

1.3 Sigmoid函数详解

Sigmoid函数(Logistic函数)公式:

σ(z)=11+e−z \sigma(z) = \frac{1}{1 + e^{-z}} σ(z)=1+e−z1

函数特点:

- 定义域:(-∞, +∞)

- 值域:(0, 1)

- 当 z=0 时,σ(z)=0.5

- 单调递增、无限平滑、可导

它的作用:

将线性回归的连续输出压缩成概率值,使模型输出具备真实的概率意义。

逻辑回归最终预测概率:

P(y=1∣x;θ)=σ(θTx)=11+e−θTx P(y=1 \mid x;\theta) = \sigma(\boldsymbol{\theta}^T \boldsymbol{x}) = \frac{1}{1 + e^{-\boldsymbol{\theta}^T \boldsymbol{x}}} P(y=1∣x;θ)=σ(θTx)=1+e−θTx1

决策规则(默认阈值0.5):

y^={1,P≥0.50,P<0.5 \hat{y}= \begin{cases} 1, & P \ge 0.5 \\ 0, & P < 0.5 \end{cases} y^={1,0,P≥0.5P<0.5

1.4 损失函数与极大似然估计

逻辑回归使用交叉熵损失(Cross Entropy Loss),而非均方误差。

单个样本损失:

Loss(y^,y)=−[ylogy^+(1−y)log(1−y^)] Loss(\hat{y}, y) = -[y \log \hat{y} + (1-y) \log (1-\hat{y})] Loss(y^,y)=−[ylogy^+(1−y)log(1−y^)]

全局损失函数:

J(θ)=−1m∑i=1m[y(i)loghθ(x(i))+(1−y(i))log(1−hθ(x(i)))] J(\theta) = -\frac{1}{m} \sum_{i=1}^m \left[ y^{(i)} \log h_\theta(x^{(i)}) + (1-y^{(i)}) \log (1-h_\theta(x^{(i)})) \right] J(θ)=−m1i=1∑m[y(i)loghθ(x(i))+(1−y(i))log(1−hθ(x(i)))]

模型训练目标:最小化损失函数,通过梯度下降求解最优参数θ。

1.5 梯度下降公式推导

损失函数对参数θ_j求偏导:

∂J(θ)∂θj=1m∑i=1m(hθ(x(i))−y(i))xj(i) \frac{\partial J(\theta)}{\partial \theta_j} = \frac{1}{m} \sum_{i=1}^m \left( h_\theta(x^{(i)}) - y^{(i)} \right) x_j^{(i)} ∂θj∂J(θ)=m1i=1∑m(hθ(x(i))−y(i))xj(i)

参数更新规则:

θj:=θj−α⋅1m∑i=1m(hθ(x(i))−y(i))xj(i) \theta_j := \theta_j - \alpha \cdot \frac{1}{m} \sum_{i=1}^m \left( h_\theta(x^{(i)}) - y^{(i)} \right) x_j^{(i)} θj:=θj−α⋅m1i=1∑m(hθ(x(i))−y(i))xj(i)

其中α为学习率。

二、Sklearn LogisticRegression 参数全解

LogisticRegression(

penalty='l2',

dual=False,

tol=0.0001,

C=1.0,

fit_intercept=True,

intercept_scaling=1,

class_weight=None,

random_state=None,

solver='liblinear',

max_iter=100,

multi_class='auto',

verbose=0,

warm_start=False,

n_jobs=None,

l1_ratio=None

)

逻辑回归参数整理

2.1 正则化相关(防过拟合)

2.1.1 penalty

正则化类型:l1/l2

l1:服从拉普拉斯分布,可实现特征筛选

l2:服从高斯分布,通用性最强

注:newton-cg、sag、lbfgs仅支持L2正则

2.1.2 C

正则化强度系数,数值越小正则约束越强,抑制过拟合效果越好

默认值1.0,仅支持正浮点数

2.1.3 tol

迭代收敛判定精度,默认1e-4,达到设定精度即终止迭代训练

2.2 模型结构(截距/常数项)

2.2.1 fit_intercept

是否为模型添加截距项b,默认开启True,日常建模推荐启用

2.2.2 intercept_scaling

仅在选用liblinear求解器且开启截距项时生效,默认取值1.0

2.3 样本不平衡/分类权重

2.3.1 class_weight

用于平衡类别差异、调整错分损失

- None:默认模式,不设置类别权重

- balanced:依据样本数量自动分配权重,样本量越少权重越高

- 自定义字典:手动设定各类别权重占比

2.4 优化求解算法(solver)

2.4.1 liblinear(默认)

坐标轴下降法,适配小数据集、二分类场景

2.4.2 newton-cg

经典牛顿法,依托二阶导数运算,迭代次数少,运算开销大

2.4.3 lbfgs

拟牛顿法,适配高维特征数据,多用于多分类任务

2.4.4 sag

随机平均梯度下降法,专门适配海量样本数据集

2.4.5 saga

sag算法升级版本,兼容L1正则,适配大数据+高维特征场景

2.5 其余辅助参数

2.5.1 dual

对偶求解模式,默认关闭;样本数量大于特征数量时固定设为False

2.5.2 random_state

随机数种子,仅在sag、liblinear算法下生效,固定实验随机结果-

三、项目环境与数据集说明

3.1 开发环境

- Python 3.11

- Pandas、Numpy

- Matplotlib

- Scikit-learn

- Jupyter Notebook

3.2 数据集介绍

数据集来源:Kaggle信用卡欺诈数据集

- 总行数:284807

- 特征数:30(V1-V28为PCA脱敏特征、Time、Amount)

- 标签:Class(0=正常,1=欺诈)

- 欺诈样本:492条,占比0.172%

数据已脱敏,无法看到原始交易信息,适合直接建模。

四、数据预处理全流程

4.1 读取数据

import pandas as pd

# 读取数据(出现编码/引擎报错可添加 encoding='utf8'、engine='python')

data = pd.read_csv("./creditcard.csv")

# 查看前5行

print(data.head())

4.2 数据脱敏说明

数据脱敏是指对敏感信息进行加密、变形、替换等处理,在不破坏数据结构与分布的前提下,保护用户隐私。本数据中V1-V28均为脱敏特征。

4.3 特征标准化(Z-Score)

Amount数值范围极大,必须标准化,保证特征权重公平。

Z标准化公式:

z=x−μσ z = \frac{x - \mu}{\sigma} z=σx−μ

代码实现:

from sklearn.preprocessing import StandardScaler

scaler = StandardScaler()

data['Amount'] = scaler.fit_transform(data[['Amount']])

4.4 删除无用特征

data = data.drop(['Time'], axis=1)

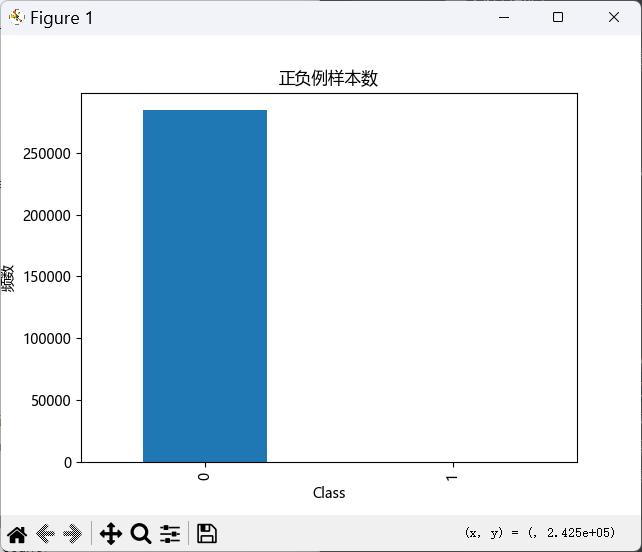

4.5 样本分布可视化

import matplotlib.pyplot as plt

from pylab import mpl

# 解决matplotlib中文显示

mpl.rcParams['font.sans-serif'] = ['Microsoft YaHei']

mpl.rcParams['axes.unicode_minus'] = False

# 统计正负样本数量

labels_count = data['Class'].value_counts()

print("样本分布:\n", labels_count)

# 绘制柱状图

plt.title("正负例样本数")

plt.xlabel("类别")

plt.ylabel("频数")

labels_count.plot(kind='bar')

plt.show()

可以清晰看到:正常样本数量碾压欺诈样本。

五、数据集划分

from sklearn.model_selection import train_test_split

# 特征与标签分离

X = data.drop('Class', axis=1)

y = data.Class

# 训练集:测试集 = 7:3,固定随机种子保证可复现

x_train, x_test, y_train, y_test = train_test_split(

X, y, test_size=0.3, random_state=1000

)

- test_size=0.3:测试集占30%

- random_state=1000:固定随机种子,保证可复现

六、基础模型训练(未调参)

from sklearn.linear_model import LogisticRegression

from sklearn import metrics

# 初始化逻辑回归(C=0.001 正则化强度)

lr = LogisticRegression(C=0.001, max_iter=1000)

# 模型训练

lr.fit(x_train, y_train)

# 训练集/测试集预测

train_predicted = lr.predict(x_train)

test_predicted = lr.predict(x_test)

# 分类报告(精确率、召回率、F1)

print("训练集分类报告:")

print(metrics.classification_report(y_train, train_predicted))

print("测试集分类报告:")

print(metrics.classification_report(y_test, test_predicted))

问题:样本不平衡导致欺诈类召回率极低,模型完全偏向多数类。

七、模型优化:交叉验证选最优C

逻辑回归中 C 是正则化强度倒数:C越小,正则化越强,防止过拟合。

使用8折交叉验证,以recall为指标选择最优C。

from sklearn.model_selection import cross_val_score

import numpy as np

# 候选C参数

c_param_range = [0.01, 0.1, 1, 10, 100]

scores = []

# 遍历C参数,交叉验证

for i in c_param_range:

lr = LogisticRegression(C=i, penalty='l2', solver='lbfgs', max_iter=1000)

# 8折交叉验证,指标为召回率recall

score = cross_val_score(lr, x_train, y_train, cv=8, scoring='recall')

score_mean = np.mean(score)

scores.append(score_mean)

print(f"C={i},平均召回率:{score_mean:.4f}")

# 找到最优C

best_c = c_param_range[np.argmax(scores)]

print(f"\n===== 最优惩罚因子 C = {best_c} =====")

八、最优模型训练与评估

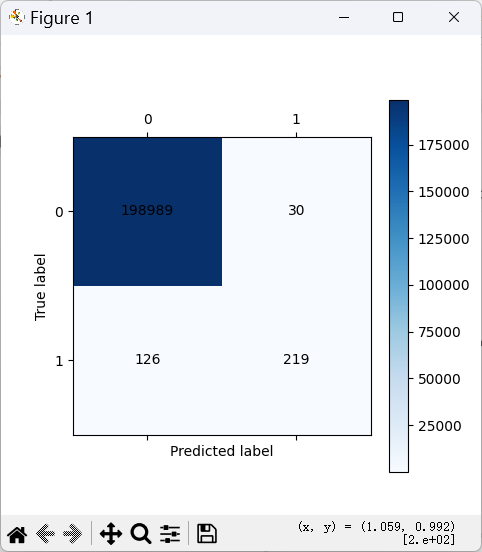

8.1 混淆矩阵可视化函数

def cm_plot(y, yp):

"""混淆矩阵可视化"""

cm = metrics.confusion_matrix(y, yp)

plt.matshow(cm, cmap=plt.cm.Blues)

plt.colorbar()

# 标注数值

for x in range(len(cm)):

for y in range(len(cm)):

plt.annotate(cm[x, y], xy=(y, x),

horizontalalignment='center',

verticalalignment='center')

plt.ylabel('真实标签')

plt.xlabel('预测标签')

return plt

8.2 训练最优模型

# 使用最优C训练

lr_best = LogisticRegression(C=best_c, penalty='l2', max_iter=1000)

lr_best.fit(x_train, y_train)

# 训练集评估

train_pred = lr_best.predict(x_train)

print("训练集分类报告:")

print(metrics.classification_report(y_train, train_pred, digits=6))

cm_plot(y_train, train_pred).show()

# 测试集评估

test_pred = lr_best.predict(x_test)

print("测试集分类报告:")

print(metrics.classification_report(y_test, test_pred, digits=6))

cm_plot(y_test, test_pred).show()

九、进阶优化:调整分类阈值

逻辑回归默认阈值为0.5,对不平衡数据不友好。

遍历阈值[0.1,0.2,...,0.9],找到召回率最优的阈值。

thresholds = [0.1, 0.2, 0.3, 0.4, 0.5, 0.6, 0.7, 0.8, 0.9]

recalls = []

for i in thresholds:

# 预测概率

y_pred_proba = lr_best.predict_proba(x_test)

y_pred_proba = pd.DataFrame(y_pred_proba)

# 只保留欺诈类概率

y_pred_proba = y_pred_proba.drop([0], axis=1)

# 自定义阈值

y_pred_proba[y_pred_proba[1] > i] = 1

y_pred_proba[y_pred_proba[1] <= i] = 0

# 计算召回率

recall = metrics.recall_score(y_test, y_pred_proba[1])

recalls.append(recall)

print(f"阈值={i},测试集召回率:{recall:.3f}")

结论:降低阈值可显著提升欺诈样本召回率,业务中可根据风控要求取舍。

十、完整代码汇总

# ==================== 1. 导入库 ====================

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

from pylab import mpl

from sklearn.preprocessing import StandardScaler

from sklearn.model_selection import train_test_split, cross_val_score

from sklearn.linear_model import LogisticRegression

from sklearn import metrics

# ==================== 2. 中文设置 ====================

mpl.rcParams['font.sans-serif'] = ['Microsoft YaHei']

mpl.rcParams['axes.unicode_minus'] = False

# ==================== 3. 数据预处理 ====================

# 读取数据

data = pd.read_csv("./creditcard.csv")

print(data.head())

# Z标准化Amount

scaler = StandardScaler()

data['Amount'] = scaler.fit_transform(data[['Amount']])

# 删除无用列Time

data = data.drop(['Time'], axis=1)

# 样本分布可视化

labels_count = data['Class'].value_counts()

print("样本分布:\n", labels_count)

plt.title("正负例样本数")

plt.xlabel("类别")

plt.ylabel("频数")

labels_count.plot(kind='bar')

plt.show()

# ==================== 4. 数据集划分 ====================

X = data.drop('Class', axis=1)

y = data.Class

x_train, x_test, y_train, y_test = train_test_split(

X, y, test_size=0.3, random_state=1000

)

# ==================== 5. 交叉验证选最优C ====================

c_param_range = [0.01, 0.1, 1, 10, 100]

scores = []

for i in c_param_range:

lr = LogisticRegression(C=i, penalty='l2', solver='lbfgs', max_iter=1000)

score = cross_val_score(lr, x_train, y_train, cv=8, scoring='recall')

score_mean = np.mean(score)

scores.append(score_mean)

print(f"C={i},平均召回率:{score_mean:.4f}")

best_c = c_param_range[np.argmax(scores)]

print(f"\n===== 最优惩罚因子 C = {best_c} =====")

# ==================== 6. 混淆矩阵函数 ====================

def cm_plot(y, yp):

cm = metrics.confusion_matrix(y, yp)

plt.matshow(cm, cmap=plt.cm.Blues)

plt.colorbar()

for x in range(len(cm)):

for y in range(len(cm)):

plt.annotate(cm[x, y], xy=(y, x),

horizontalalignment='center',

verticalalignment='center')

plt.ylabel('真实标签')

plt.xlabel('预测标签')

return plt

# ==================== 7. 最优模型训练与评估 ====================

lr_best = LogisticRegression(C=best_c, penalty='l2', max_iter=1000)

lr_best.fit(x_train, y_train)

# 训练集

train_pred = lr_best.predict(x_train)

print("训练集分类报告:")

print(metrics.classification_report(y_train, train_pred, digits=6))

cm_plot(y_train, train_pred).show()

# 测试集

test_pred = lr_best.predict(x_test)

print("测试集分类报告:")

print(metrics.classification_report(y_test, test_pred, digits=6))

cm_plot(y_test, test_pred).show()

# ==================== 8. 阈值优化 ====================

thresholds = [0.1,0.2,0.3,0.4,0.5,0.6,0.7,0.8,0.9]

for i in thresholds:

y_pred_proba = lr_best.predict_proba(x_test)

y_pred_proba = pd.DataFrame(y_pred_proba).drop([0], axis=1)

y_pred_proba[y_pred_proba[1] > i] = 1

y_pred_proba[y_pred_proba[1] <= i] = 0

recall = metrics.recall_score(y_test, y_pred_proba[1])

print(f"阈值={i},召回率={recall:.3f}")

十一、模型评估指标详解

11.1 混淆矩阵

- TP(真正例):预测欺诈,实际欺诈

- FN(假反例):预测正常,实际欺诈

- FP(假正例):预测欺诈,实际正常

- TN(真反例):预测正常,实际正常

11.2 核心指标

准确率:Accuracy=(TP+TN)/(TP+TN+FP+FN)

精确率:Precision=TP/(TP+FP)

召回率:Recall=TP/(TP+FN)

F1 值:F1=2×(Precision×Recall)/(Precision+Recall)

AtomGit 是由开放原子开源基金会联合 CSDN 等生态伙伴共同推出的新一代开源与人工智能协作平台。平台坚持“开放、中立、公益”的理念,把代码托管、模型共享、数据集托管、智能体开发体验和算力服务整合在一起,为开发者提供从开发、训练到部署的一站式体验。

更多推荐

10

10 0

0- 0

已为社区贡献10条内容

已为社区贡献10条内容

所有评论(0)